now loading...

China’s economy today bears an unsettling resemblance to Japan’s in the 1990s, when the collapse of a housing bubble led to prolonged stagnation. But Japan’s “lost decades” were not the inevitable result of irreversible trends; they reflected policy blunders, rooted in a flawed understanding of the challenges the economy faced. Will Chinese policymakers make the same mistakes?

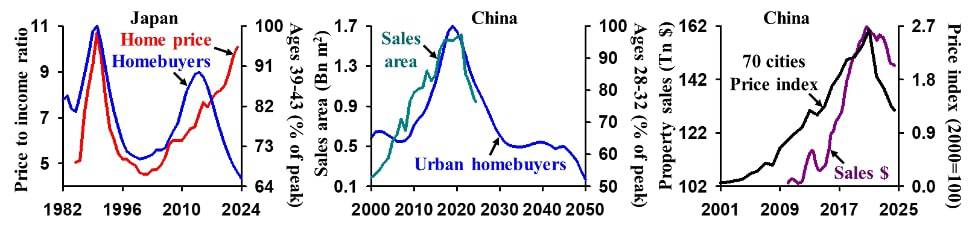

Japan’s housing bubble was preceded by sharply rising ratios of home prices to annual income, with Tokyo’s surging from eight in 1985 to 18 in 1990. This trend was driven by a number of factors, including Japan’s land-tax policy, financial deregulation and poor coordination of fiscal and monetary policy. But demand from first-time homebuyers – aged 39-43, on average – also made a substantial contribution.

Because homeowners felt wealthier, they consumed more. This drove up the prices of goods, services, and stocks, leading to more jobs and less unemployment. But demand for new housing soon began to fall, and demographic shifts were a key factor. In 1991, as the share of Japan’s population aged 65 and older reached 13%, the number of first-time homebuyers began to decline. Property values plummeted, the stock market collapsed, and Japan fell into a deflationary trap, characterized by falling fertility and rising unemployment.

A misdiagnosis of the problem made matters much worse: what was actually a chronic demographic disease was treated as an acute illness. Policymakers believed that Japan was grappling with yen appreciation as a result of the 1985 Plaza Accord, under which the world’s major economies agreed to devalue the dollar. So, to stem the currency’s rise, they printed money, lowered interest rates, increased the government deficit, and engaged in quantitative easing.

These policies, together with the rebound in the number of new homebuyers that began in 2001, caused home prices to start rising again – and exacerbated the underlying disease. As starting a family became more expensive, young people delayed marriage and had fewer children. The government tried to boost birth rates with interventions like increased child allowances and improved childcare services, but it achieved only limited success: the fertility rate rose from 1.26 births per woman in 2005 to a mere 1.45 a decade later.

At that point, then-Prime Minister Abe Shinzō set the goal of lifting the fertility rate to 1.8. But the relevant measures – which sought, for example, to make it easier for women to return to work after giving birth – could not offset the effects of the accommodative monetary policies that were viewed as vital to combat deflation and stimulate economic growth. Home prices continued to soar, marriages declined further, and births plummeted. Last year, Japan’s fertility rate amounted to just 1.15 births per woman.

In the past, Japan welcomed low interest rates and a weak yen, because its economy was highly dependent on exports. But the ageing and shrinking of its labour force have generated upward pressure on wages, fuelling domestic inflation, weakening manufacturing, and transforming Japan from a surplus country into a deficit country, thereby making it vulnerable to imported inflation. So, Japan has escaped its deflationary trap only to become ensnared in a long-term inflationary trap, which, by reducing purchasing power and parenting capacity, will reduce fertility further. By fuelling a demographic collapse, Japan’s approach to ending its “lost decades” has set the stage for “lost centuries”.

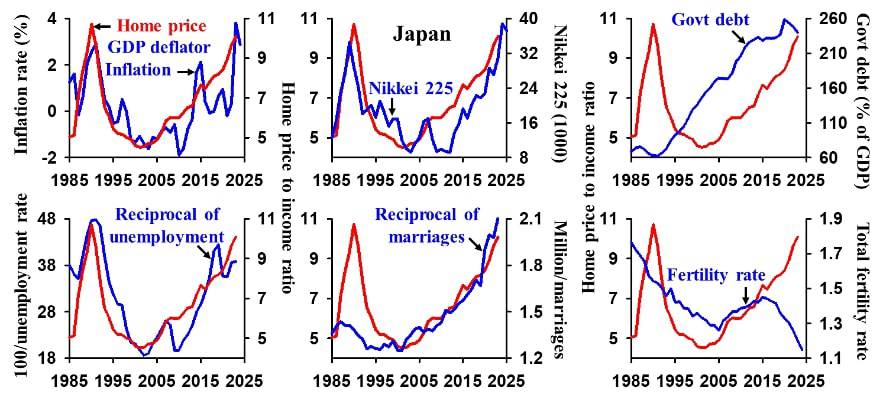

This should serve as a cautionary tale for China, which is confronting real estate and demographic crises of its own. In recent decades, rapid urbanization, policy-induced artificial land scarcity, the dependence of local governments on land sales for revenue, and heady expectations of future growth caused real-estate prices to soar. Strong demand from first-time homebuyers also helped: since young Chinese typically have no siblings, owing to decades of fertility restrictions, they tend to purchase their first home about 11 years earlier than their Japanese counterparts.

But the number of Chinese urban dwellers aged 28-32 peaked in 2019 – and the real-estate bubble burst shortly thereafter. Now, the real estate sector – which, at its 2020-21 peak, contributed 25% of total GDP and 38% of government revenue – is blighted by weak demand, falling construction and severe overcapacity. Declining prices have decimated household wealth, with losses equivalent to China’s annual economic output. This has undermined consumption, employment, borrowing and investment.

The crisis that is brewing in China is more severe than the one Japan faced. For starters, China’s housing bubble is much larger. For example, residential investment, as a share of GDP, was about 1.5 times higher in China in 2020 than in Japan in 1990. Property accounted for about 70% of Chinese households’ total assets in 2020, compared to around 50% in Japan in 1990. China’s price-to-income ratio today is more than twice that of Japan in 1990.

Moreover, China’s fertility rate is lower. Whereas Japan experienced a second surge of first-time homebuyers a decade after the first, China can look forward to no such thing. The share of the population over the age of 65 is increasing much faster in China than it did in Japan: it took Japan 28 years to get where China will get between now and 2040. During that period ( 1997-2025 ), Japanese GDP growth averaged just 0.6% annually.

Finally, China faces much greater deflationary and unemployment pressures than Japan did. Chinese household consumption accounted for only 38% of GDP in 2020, compared to 50% in Japan in 1990.

But perhaps the most ominous portent is that China’s government continues to tout a potential growth rate of 5%, with some prominent figures suggesting that it could achieve rates as high as 8%. To get there, policymakers are pursuing measures with high short-term returns – such as expanding the supply of affordable housing and carrying out quantitative easing – while all but ignoring the economy’s weak fundamentals. As Hegel famously put it, “The only thing we learn from history is that we learn nothing from history.”

Yi Fuxian is a senior scientist at the University of Wisconsin-Madison.

Copyright: Project Syndicate